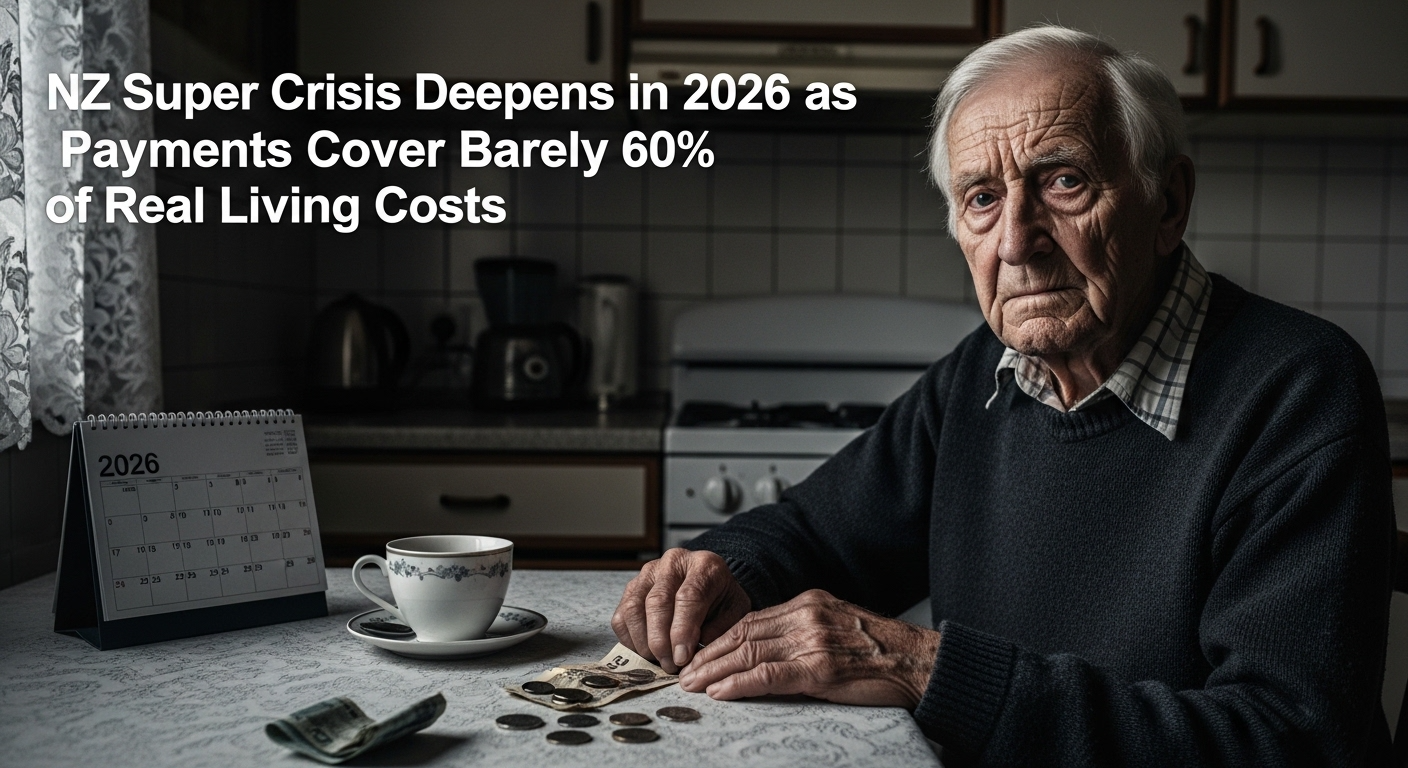

A serious retirement affordability crisis is unfolding across New Zealand in 2026.

Fresh analysis suggests that NZ Super payments now cover only around 60% of real living costs for many retirees.

For thousands of older citizens, that gap is no longer manageable.

Living Costs Rising Faster Than NZ Super

Over recent years, essential expenses have climbed steadily.

Housing, electricity, food, insurance, and healthcare costs have all increased at a faster pace than pension adjustments.

While New Zealand Superannuation is linked to wage growth, retirees say it no longer reflects real household inflation.

For many, every month feels tighter than the last.

The 60% Reality in 2026

Financial modelling shows a growing shortfall between pension income and basic needs.

When total essential costs are calculated, NZ Super often covers just six out of every ten dollars required for a modest lifestyle.

That leaves retirees relying on savings, family support, or cutting back on essentials.

For those without assets, the pressure is severe.

What Everyday Costs Look Like for Pensioners

A single retiree living alone faces significant monthly expenses.

Housing remains the largest cost, whether renting or paying rates on a home.

Food prices have risen sharply, especially fresh produce and meat.

Healthcare and electricity bills continue to climb.

Combined, these essentials absorb nearly all pension income.

Income vs Essential Expenses in 2026

Below is a simplified comparison reflecting average annual figures for a single pensioner.

| Category | Approximate Annual Amount (NZD) |

|---|---|

| NZ Super after tax | $31,000 |

| Housing and rates | $15,500 |

| Food and groceries | $8,000 |

| Electricity and utilities | $4,200 |

| Healthcare and transport | $4,500 |

| Total essential living costs | $32,200 |

| Estimated shortfall | -$1,200 |

This narrow margin shows how little buffer remains.

Unexpected bills can quickly push retirees into hardship.

Housing Driving the Financial Strain

Housing costs are the biggest pressure point.

Renters face rising rents with limited stability.

Homeowners deal with higher rates, insurance premiums, and maintenance costs.

Older properties often mean higher power bills due to poor insulation.

Heating during winter becomes a difficult decision for many.

Fixed Income Means Limited Options

Retirees typically have limited ways to increase income.

Health conditions often prevent part-time work.

Savings may already be depleted.

When costs rise unexpectedly, there is little room to adjust.

Even small price increases create real stress.

Health Consequences of Financial Stress

Financial pressure is increasingly linked to health risks.

Some pensioners delay medical appointments to save money.

Others reduce heating during cold months.

Cold homes contribute to respiratory issues and hospital visits.

Mental wellbeing also suffers when insecurity becomes constant.

Regional Gaps Are Widening

Not all regions experience the crisis equally.

Retirees in colder areas face higher energy bills.

Urban pensioners often deal with expensive housing.

Rural residents face increased transport costs and limited services.

The same pension payment stretches very differently depending on location.

Government Support Not Closing the Gap

Several programmes provide temporary assistance.

Winter energy support helps during colder months.

Accommodation supplements assist renters.

However, many retirees say these measures no longer bridge the affordability gap.

Support often disappears as quickly as it arrives.

Growing Calls for Pension Reform

Economists and advocacy groups are urging reform.

Some suggest linking NZ Super adjustments more closely to essential cost inflation.

Others propose targeted housing or energy supplements.

Healthcare affordability is also a growing focus.

Without structural change, the shortfall may continue expanding.

The Human Side of the Numbers

Behind the data are real stories.

Retirees describe budgeting down to the dollar.

Many monitor electricity usage daily.

Some rely on family for groceries or repairs.

Others avoid asking for help due to pride.

The emotional toll is just as significant as the financial one.

An Ageing Population Adds Urgency

New Zealand’s population is steadily ageing.

More people will depend on NZ Super in coming years.

Longer life expectancy means pensions must stretch further.

If payments remain misaligned with real costs, pressure will intensify.

The issue is not temporary.

Why 2026 Is a Turning Point

The 60% coverage figure has become a warning signal.

It highlights the gap between policy assumptions and real-world expenses.

Retirement security was meant to guarantee dignity.

Instead, many older citizens face constant financial juggling.

This moment is forcing renewed debate about adequacy.

What Retirees Are Doing Now

Many pensioners are adjusting spending habits.

They compare grocery prices carefully.

They delay non-urgent purchases.

They limit travel and social activities.

These sacrifices protect survival, but reduce quality of life.

Looking Ahead

The future of NZ Super will likely remain a major policy topic throughout 2026.

If living costs continue rising faster than payments, pressure for reform will grow stronger.

Ensuring retirement dignity is not only an economic issue.

It is a reflection of national values.

For now, thousands of retirees continue balancing essential bills against limited income, hoping meaningful change arrives before the gap widens further.

Read more: https://onetreegrill.site/